- Over 90% of UK investor portfolios are underperforming due to inefficiencies - learn how to unlock their growth potential.

- Are restricted advisers holding you back? Discover why independence in financial advice is critical for portfolio success.

- Maximise FSCS protection by optimising fund management diversity - How to ensure your investments are safeguarded.

- Active vs Passive Investing: Uncover the strategic balance that drives consistent and superior returns.

- Self-managing or professional advice? Avoid common pitfalls and make informed choices to enhance your portfolio performance.

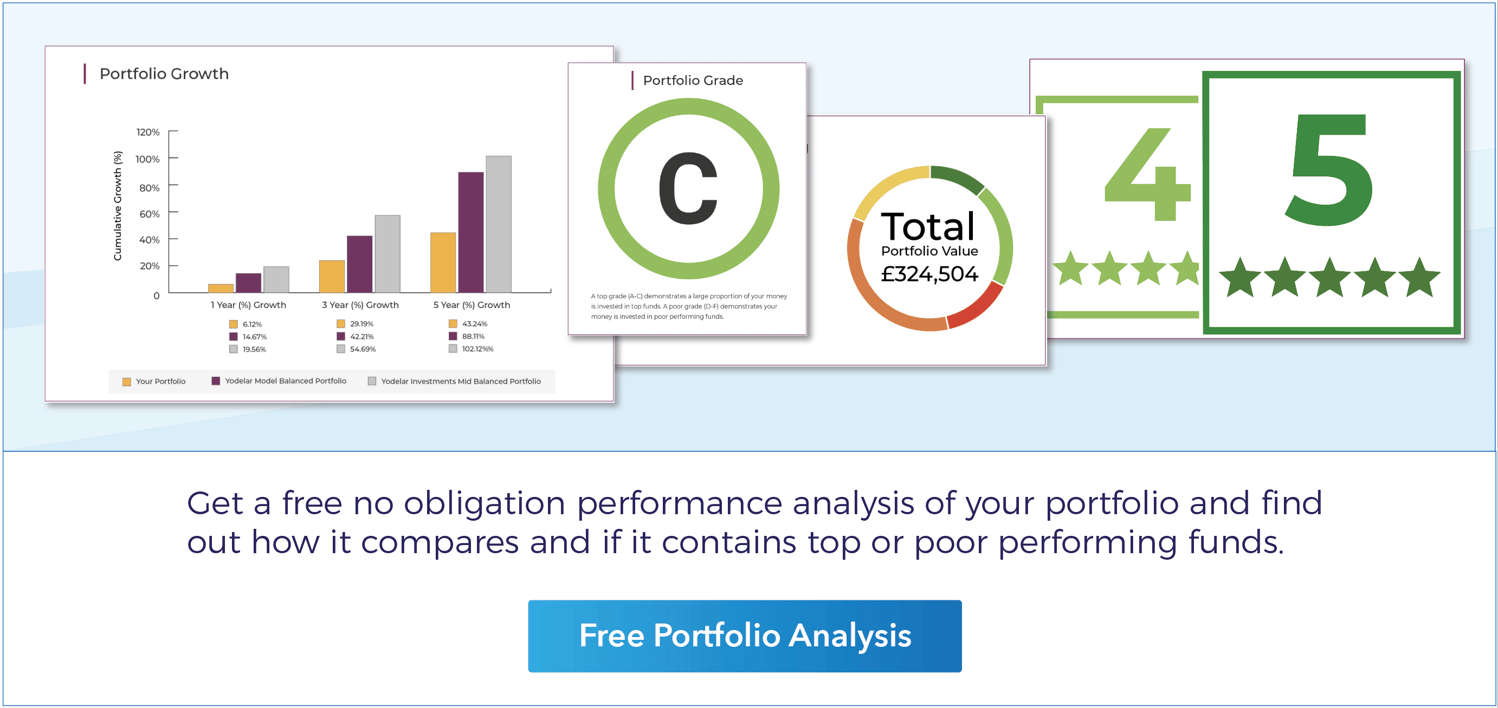

For years, Yodelar has analysed the performance and quality rating of portfolios for thousands of UK investors. Our extensive analysis has uncovered that over 90% of investors hold portfolios containing inefficiencies that stunt growth potential, resulting in many UK investors to miss out on enhanced portfolio growth.

Inefficient investing can have adverse long-term consequences, making it crucial to identify and correct any portfolio deficiencies.

Below are the 8 most important points you need to consider as an investor to get the most from investing.

1. Restricted or Independent Advice?

If your current investments are managed by a restricted advice firm, there is likely considerable scope to enhance the efficiency and performance of your portfolio.

No single fund manager consistently dominates top performance across all asset classes. However, restricted advice firms often confine their clients to portfolios built solely from their in-house range of funds. This inherently limits investor choice and flexibility, leaving portfolios unable to fully capitalise on top performing funds available in the broader market.

Such restrictions can severely impair the ability to optimise portfolio performance. By focusing exclusively on their own funds, restricted advice firms overlook the competitive advantages offered by other fund managers, ultimately hampering the potential for consistent, long-term growth across diversified asset classes.

The Importance of Independent Financial Advice

Independent Financial Advisers (IFAs) have the ability to consider and recommend a wide range of investment funds from across the market, providing unbiased and unrestricted advice tailored to their clients' needs and objectives. In contrast, restricted advisers often use their restricted status to promote their own products, platforms, and investment funds.

These firms may earn higher margins by selling their own products, while exposing clients to a limited range of potentially poor performing and more expensive options.

Benefits of Unrestricted Investment Advice

We strongly believe that having the freedom to explore the market without being tied down to fund managers allows investors to take a versatile approach to investing. This freedom enables investors and their advisers to select funds based on merit, which we believe is important in obtaining high level portfolio efficiency.

Additionally, research by the Personal Finance Society and NextWealth, found clients of restricted advisers pay on average 0.28% more in overall charges than those who invest with independent financial advisers.

2. Fund Performance

Evaluating fund performance is a crucial metric for investors and advisory firms. Although past performance does not guarantee future results, it can provide valuable insights into which fund managers and funds have outperformed or underperformed their sector peers.

When presented with the option, investors would prefer to invest with fund managers that consistently perform over varying time frames in the top 25% in their sectors versus fund managers that perform in the worst 25% of performers.

Consistency is a key indicator of success and is central to our portfolio management approach. We believe consistency displayed by investment funds that maintain a high sector ranking over numerous market cycles reflects efficiency and expertise from the fund manager through their ability to deliver competitive returns for their clients over both the short and long term. While short-term political and economic fluctuations can make it difficult for even the best fund managers to consistently outperform their peers, analysing performance over 1, 3, and 5-year periods can highlight those who excel in particular markets.

Funds that consistently rank well in their sector indicate strong management expertise, whereas those that consistently rank poorly suggest an inability to deliver competitive returns for investors.

There are 3 important fund performance considerations:

Comparative Benchmarking

The performance of each fund can be assessed relative to competing peer group funds classified within the same sector. This comparative analysis across multiple time horizons provides insights into a fund’s overall quality and the capabilities of its management team.

Managerial Skill

Historical returns indicate a fund’s effectiveness and the competencies of its managers. Funds that consistently rank high within their sectors typically demonstrate a significant level of expertise. Conversely, fund managers overseeing consistently underperforming funds demonstrate a lack of quality and an inability to deliver competitive returns. While past performance alone cannot predict future returns, it remains a valuable tool for assessing manager skills.

Navigating Market Cycles

Over a multi-year span, investments encounter various economic and political environments. The ability of a fund and its managers to navigate these cycles offers valuable clues about their competence and abilities.

3. Government Financial Services Compensation Scheme (FSCS)

Many investors are not aware that investment funds are also protected by the Governments Financial Services Compensation Scheme to a maximum value of £85,000 per provider. Its purpose is to protect investors should an investment firm who is responsible for managing a fund fail or be unable to pay claims against it.

Maximising Protection Under the Financial Services Compensation Scheme is available to most investors, however many investors are unaware they are not optimising this protection as their portfolios often contain funds managed by as little as 1 fund management brand, thus limiting their protection.

By diversifying your portfolio to include funds from several different fund management brands can help add a greater layer of protection to your investments.

The Financial Services Compensation scheme administered by the Government allows you to enter your details to identify what level you are protected too, they are also available for online chat:

https://www.fscs.org.uk/check/

4. Unbiased Investing

It’s important to understand that financial advisers do not hold clients’ money directly. Instead, investments are held by the fund management companies managing the individual funds within the portfolio. As a result, the failure of an advisory firm does not directly impact investors’ holdings. However, the concentration of funds within a single management group can introduce additional risks, particularly if that group encounters financial difficulties.

Partnering with an adviser who proactively manages provider risk by diversifying investments across multiple fund managers can provide significant value to investors. A well-diversified portfolio ensures broader market coverage, reduces reliance on any one provider, and enhances FSCS protection

No single fund management group consistently delivers top-performing funds across all sectors or markets. Therefore, an impartial, evidence-based investment approach is critical. This involves identifying specialist funds tailored to specific sectors, regions, and industries, as well as fund managers with proven expertise in their respective domains. Such an approach can significantly improve portfolio quality by focusing on:

Diversifying manager risk: Spreading investments across multiple fund managers to mitigate the impact of any single provider underperforming.

Utilising specialist funds: Selecting funds managed by experts with a deep understanding of specific sectors or regions.

Making fact-based investment decisions: Prioritising data-driven insights over perception or brand loyalty to build a robust, high-performing portfolio.

This strategic approach helps to ensure portfolios are resilient but also better optimised for growth and risk management.

5. Passive & Active Investing

When deciding which type of funds to invest in, one of the key choices investors face is between passive and actively managed funds. While this may seem like a straightforward decision, it has sparked considerable debate among investors for years, with many strongly favouring one approach over the other.

Passive funds aim to replicate the performance of a specific index, offering a cost-effective, hands-off approach. Conversely, actively managed funds rely on the expertise of fund managers to make strategic decisions with the goal of outperforming the market, though they typically come with higher management fees.

Each approach has its merits. Passive funds are often favoured for their lower costs and ability to deliver consistent, market-matching returns. Meanwhile, active funds are lauded for their potential to outperform the market, particularly in specific sectors or under unique market conditions. However, the key is to avoid being constrained by allegiance to one strategy. Passive investing provides a cost-effective and stable foundation, particularly for long-term investors, while active investing offers the flexibility to capitalise on opportunities for outperformance in targeted areas.

A recent review we completed of 3,637 funds identified that 57% of active funds underperformed their sector averages over five years, while only 40% of passive funds did so, underscoring the stability of passive strategies. Nevertheless, actively managed funds were more likely to secure top positions in their sectors, with high performers such as the Royal London Global Equity Select M Fund achieving returns of 135.86% over five years, far exceeding the IA Global sector average of 54.27%.

This contrast highlights the risks of overcommitting to a single approach. Investors who rely exclusively on passive funds may miss out on the significant outperformance potential of active strategies in certain market conditions or sectors. Similarly, those who focus solely on active funds expose themselves to higher costs and a greater likelihood of underperformance. By limiting themselves to one strategy, investors narrow their options and risk forgoing a balanced approach that leverages the strengths of both. This factor alone highlights the importance of partnering with the right advisor who has an understanding of fund performance and can help determine the most suitable portfolio balance.

Related Article: Passive Vs Actively Managed Funds : A Performance Comparison

6. Advice Versus Self Investing

An increasing number of investors are returning to professional advice, reversing the trend from a decade ago when the rise of fund supermarkets and technological advancements prompted a shift towards self-managed investing. Today, the limitations and risks associated with self-investing are becoming more apparent.

Key challenges faced by self-investors include:

(i) Ineffective Risk Management

Many self-investors fail to maintain an efficient asset allocation model or rebalance their portfolios regularly. Over time, higher-risk funds often outperform lower-risk ones, causing an unintended drift towards an overly aggressive risk profile. This imbalance can leave portfolios dangerously exposed during market downturns. Moreover, self-investors often lack the tools and expertise to thoroughly assess the underlying holdings and risk levels of their chosen funds.

(ii) Poor Fund Selection Criteria

A significant number of self-investors choose funds based on marketing influence rather than merit. High-profile cases, such as the now defunct Woodford Equity Income fund, exemplify the pitfalls of selecting investments without evaluating key factors like fund performance, underlying holdings, and the track record of the fund manager.

(iii) Underperforming Funds

Self-investors frequently neglect to evaluate the historical performance of fund managers. As a result, portfolios may include persistently underperforming funds, further diminishing growth potential.

By partnering with high-quality, research-driven advice firms, investors can mitigate these risks. Professional advisers ensure portfolios are strategically rebalanced to align with individual risk profiles and are constructed with top-performing, data-backed funds to maximise growth and resilience.

Related Article - Self Investing Versus Advice

7. Quality Control - Maintaining A Top Quality Investment Strategy

Successful investing requires a focus on growth, and quality firms prioritise this by building strategies around high-performing funds and fund managers with a consistent history of outperforming the market. This evidence-based approach allows them to focus on what truly matters - maintaining independence, exercising disciplined decision-making, and fostering a long-term perspective.

A quality-driven investment strategy is essential for achieving the best outcomes over the medium to long term. While investing can present numerous challenges, focusing on key principles, such as those outlined in this article, can significantly enhance portfolio value when managed effectively.

Quality investment firms follow efficient, research-led processes to ensure their portfolios adhere to best practices. Such portfolios are the result of years of rigorous analysis, involving the assessment of hundreds of fund managers and thousands of investment options. Research consistently shows that only a small proportion of funds and fund managers deliver top-tier performance, with the majority of portfolios containing underperforming funds that can hinder growth.

By leveraging this research, quality firms construct strategically balanced, risk-rated portfolios built exclusively with high-performing funds across all asset classes. These portfolios are designed to optimise growth potential while maintaining an appropriate level of risk for each investor.

For investors seeking to grow their wealth efficiently, partnering with a firm that implements data-driven strategies and adheres to best practices can provide a significant advantage. These firms offer a long-term perspective, focus on quality investments, and ensure portfolios are optimised to deliver consistent performance.

Discover how we can help you grow your wealth efficiently - Book a no-obligation call with a Yodelar Investments Adviser.

8. Important: Shopping Around - Knowing What To Look For

Many new potential clients that come to Yodelar are unhappy with their existing returns, the advice they have received to date, or the results they have had from self managing their investments. We often hear from investors that they are shopping around prior to making a decision.

That is great, and always welcome but the biggest issue (and we see this a lot) is that they do not know what they are shopping for i.e. they have not drawn up a list of what is important to invest efficiently. The result is they may not be able to identify and partner with the most suitable adviser.

For your convenience we have created a shopping list that will help.

- Whole of market access to all funds/managers (not restricted)

- Clear defined risk models

- Can demonstrate the performance of the funds recommended

- Have knowledge of the investment sectors and performance within each

- Have a clear, transparent charging structure

- Clearly defined service management structure that includes regular portfolio rebalances and reviews with defined reporting timeframes.

- Avoid recommendations to invest in unregulated investments such as Bitcoin, and all other cryptocurrencies, Mini-bonds, Peer-to-peer investments

- Always check a firm's status on the Financial Services Register

Optimise Your Investments With Yodelar

Investing, like many aspects of life, isn't always straightforward and for some it can be more uncomfortable and stressful than others. As an investor, you will always be exposed to factors that can cause values to rise and fall. Investing can result in emotional decision making, but the investors who reach their objectives efficiently are typically those who have a disciplined and pragmatic approach to investing, and follow a structured, long term strategy. When this is followed better outcomes can be achieved.

Book a no obligation call with one of our advisers to learn more about your options and find out how we can help you improve your portfolio returns.